Gain-of-Function Monetary Policy

Description

As we saw during the covid pandemic, when lab-created experiments escape their confines, they can wreak havoc in the real world. Once released, they cannot easily be put back into the containment zone. The “extraordinary” monetary policy tools unleashed after the 2008 financial crisis have similarly transformed the U.S. Federal Reserve’s policy regime, with unpredictable consequences. The Fed’s new operating model is effectively a gain-of-function monetary policy experiment.

That was Treasury Secretary Scott Bessent last spring in a piece for The International Economy magazine under the headline, “The Fed’s New ‘Gain-of-Function’ Monetary Policy.”

It was timely considering the recent histrionic calls to keep the Fed “independent” over the attempted firing of Federal Reserve Board Governor Lisa Cook and President Trump’s name-calling of Fed Chairman Jerome “Too Late” Powell. Maybe it’s time to ask: should the Fed get to do whatever it wants? While it’s true that presidents appoint board members, who are then approved by the U.S. Senate, should that also mean the central bank can play God with the nation’s economy?

Bessent argues that the Fed’s policy response to both the 2008 financial crisis and the 2020 pandemic amounted to “gain of function” experiments that escape the lab.

The Fed deployed a combination of sustained, near-zero short-term interest rates (Fed Funds) and a practice known as quantitative easing (QE) to “save” our economy. Unfortunately, perhaps like the Covid mRNA vaccines, the Fed had little idea what the long-term effects would be from this untested cocktail of policy medicine. Also, like the Covid vaccine, the Fed has turned its unconventional emergency response into just another tool in its kit.

The Fed’s actions had major ramifications, both positive and negative, yet they were made with relative ease. Then-Treasury Secretary Hank Paulson coordinated with the Fed in 2008, but there was no pushback or internal levers to stop their major policy decisions. Unlike the Supreme Court, where members can issue strongly-worded dissent opinions, it’s only by reading the minutes of Fed meetings that we can get a sense of what little dissent there is, as was the case in 2010, when Thomas Hoenig was the lone member to object to continuing near-zero interest rates.

The Policies: ZIRP and QE

The Fed pretty much maintained ZIRP (Zero Interest Rate Policy) until 2017 and then again from 2020 to 2022 in response to the pandemic. This punished people who put their money in savings accounts, money market accounts, and CDs — particularly retirees who need relatively risk-free interest income.

Meanwhile, it was manna from heaven for the highly leveraged players: the hedge funds, private equity funds, leveraged buy-out funds and financial institutions. Borrowed money is their oxygen. Private equity and its kissing cousin, private credit, would not be the colossuses they are today without it.

Then there’s quantitative easing. This is where the Fed boldly went in 2008 where it had never gone before. Until then, the policy was dismissed because it’s similar to a central bank printing money, which is what Germany’s Weimar Republic did, if that tells you anything.

The difference with QE is that instead of printing money, the Fed creates digital reserves to buy assets.

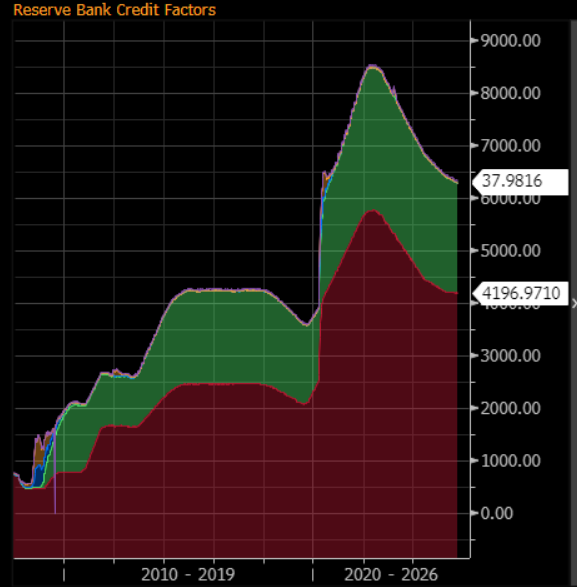

In 2008, however, after the Fed failed to recognize the subprime mortgage crisis that turned into a financial and economic catastrophe, it embarked on QE by buying trillions of dollars of U.S. Treasury notes and bonds, and Fannie Mae, Freddie Mac and Ginnie Mae mortgage-backed securities (Agency MBS). The Fed did two major buying rounds of QE, first beginning in 2008 in response to the financial crisis and then again in 2020 in response to the pandemic. At its height, the Fed owned more than $8.5 trillion in Treasuries and Agency MBS — 20% of the Treasuries market and one-third of Agency MBS!

Federal Reserve Balance Sheet

Quantitative Easing Explained

Yes Virginia, the Fed created new money, and lots of it.

The way QE worked, also known in Fedspeak as POMO (Permanent Open Market Operations), was the Fed on most mornings would ask both U.S. Treasury and Agency MBS dealers (i.e., big banks) to offer them say, $3 billion of Treasuries and $2 billion of Agency MBS. By late morning, the Fed was the proud owner of another $5 billion in bonds. Wash, rinse and repeat every day. The Fed paid for these daily gargantuan purchases by electronically “printing” money and wiring it to the banks’ reserve accounts at the Fed. The Fed paid interest to the banks to encourage them not to withdraw this “new money” they were paid. It was the first time the Fed paid interest on what it calls “excess reserves.”

The Fed’s massive buying pushed up prices of these bonds. When prices go up, yields go down. The first chart below shows the immediate effect QE had on Treasury yields (represented by the 10-year Treasury yield). The second chart shows Agency MBS yields (represented by the Fannie Mae 30-year Current Coupon yield).

United States

United States