Pivot Hopes on Hold

Description

Investor optimism for a year-end rally faded as inflation worries and geopolitical shocks overtook an early burst of relief. The 43-day U.S. government shutdown ended mid-week, briefly lifting sentiment that the Federal Reserve still had room to cut rates in December.¹ Stocks attempted a rebound, but tariff-driven price pressures and a late-week jump in oil quickly soured the mood.²³ By Friday, major indexes were essentially flat, reflecting a market caught between relief and anxiety.³

Inflation vs. the Fed

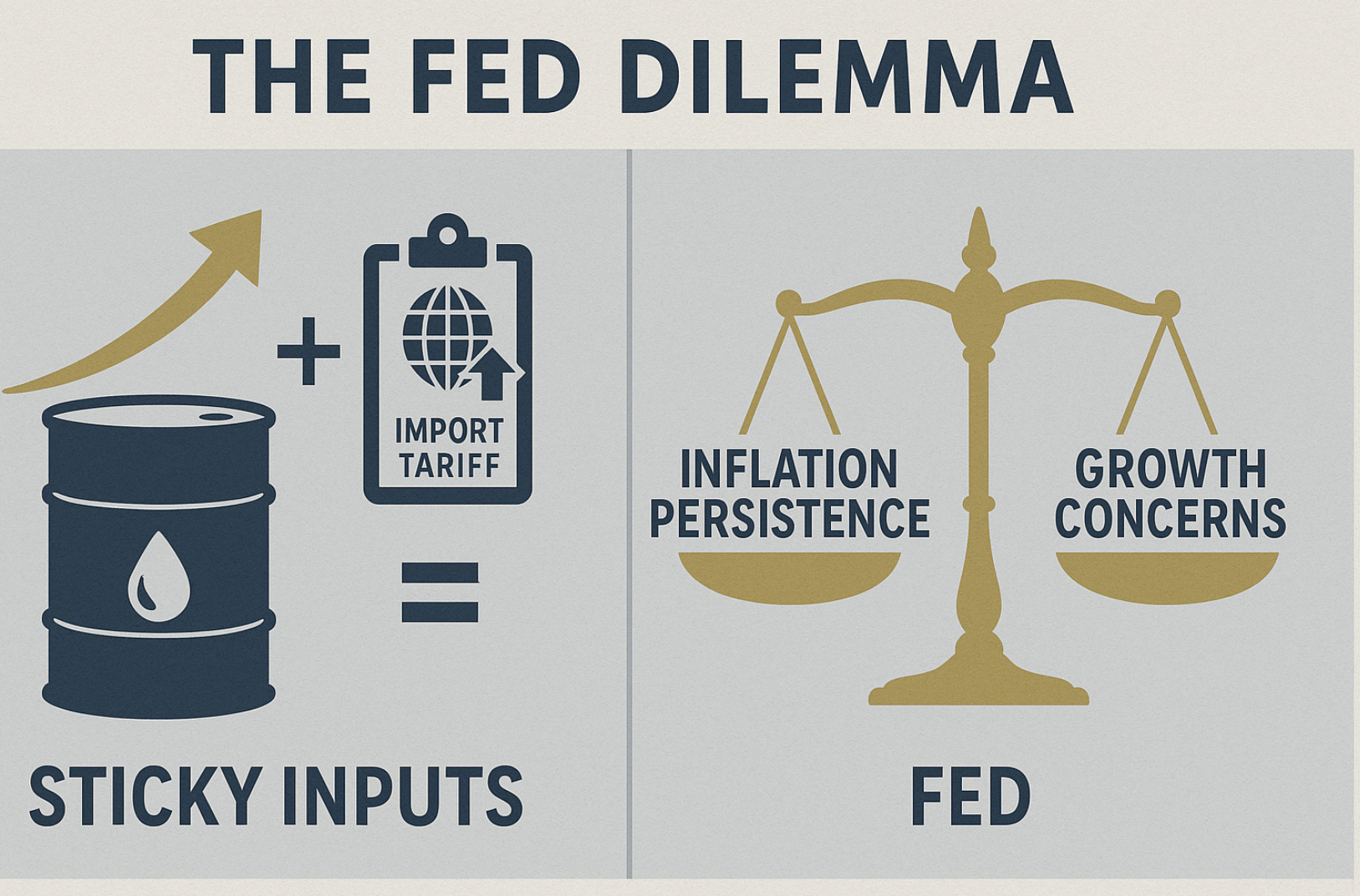

With official data delayed by the shutdown, traders turned to proxies and found little comfort. The Cleveland Fed’s “nowcast” suggested inflation was still running near a 3% annual pace—well off the 2022 highs but still above the Fed’s 2% target.¹ Tariffs under President Donald Trump continued to feed into higher costs for imported goods.² Then a Ukrainian drone attack on a key Russian Black Sea export hub sent crude oil up more than 2%, reviving concerns that energy prices could keep inflation sticky.³

Early in the week, many on Wall Street still expected another rate cut in December. A Reuters poll showed 80% of economists anticipating a quarter-point move, which would mark the Fed’s third straight reduction.⁴ But a series of hawkish comments from Fed officials quickly undermined that view. Several policymakers argued that inflation remained “too hot,” signaling skepticism about further easing.³ Market-implied odds of a December cut fell from roughly 67% to below 50% in just a few days.³ The “Santa Claus cut” narrative gave way to a more cautious assumption that the Fed might pause and wait for clearer evidence that inflation is truly on track.

Valuation worries compounded the tension. Mega-cap AI beneficiaries—such as Nvidia and its peers—now account for more than a quarter of the S&P 500 by market cap, up from under 15% only a few years ago.² That concentration leaves the broader market more vulnerable if its biggest winners stumble.

United States

United States