US Market Open: Sentiment hit after China's MOFCOM takes action against US firms

Update: 2025-10-14

Description

- China's MOFCOM announced that it is taking countermeasures against five US-linked firms; said the US cannot have talks while threatening new restrictions.

- French PM Lecornu's government is to present a budget aiming to reduce the deficit to 4.7% by end-2026, according to La Tribune.

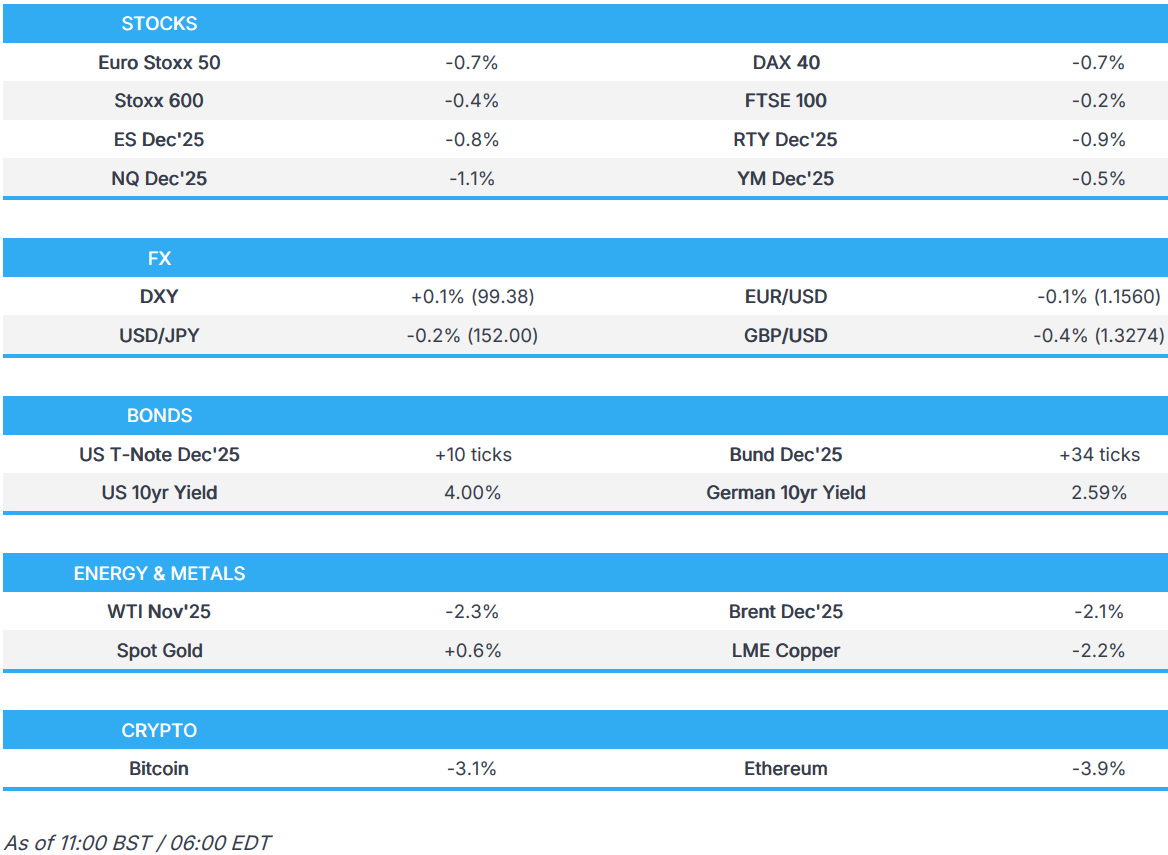

- Equities lower across the board, as markets digest the latest trade-related escalations by China on the US; traders also await a number of US earnings.

- JPY benefits from haven bid, GBP hit by soft jobs, Antipodeans dented by risk-tone.

- Global paper firmer amid the weakened risk tone, Gilts lead after data, OATs await PM Lecornu.

- Crude benchmarks fall as Middle East tensions ease, XAU pulls back from new ATHs.

- Looking ahead, US NFIB (Sep), Fed Discount Rate Minutes, Speakers including ECB’s Villeroy, Kocher, BoE’s Bailey & Taylor, Fed’s Powell, Waller, Collins & Bowman, BoC’s Rogers, RBA’s Hunter & Hauser, RBNZ’s Conway. Earnings from JPMorgan, Goldman Sachs, Citi, Wells Fargo, Johnson & Johnson & LVMH.

</figure>

</figure>TARIFFS/TRADE

- China officially began special port fees for US ships, while it was earlier reported that China issued implementation rules on port fees on US ships and exempted China-made ships owned by US companies from port fees, while it is to adjust special port fees on US ships as needed.

- China's MOFCOM responded to the US saying it has proposed talks with China after rare earth restrictions, in which MOFCOM stated the US cannot have talks while threatening to intimidate and introduce new restrictions, which is not the right way to get along with China, while it urged the US to correct its “wrong practices” as soon as possible and show sincerity in talks with China. It also stated that export curbs are not an export ban and do not prohibit exports. Furthermore, it said they held working-level talks on Monday and noted that both sides have maintained communication under the framework of the China-US economic and trade consultation mechanism. However, MOFCOM later announced that it is taking countermeasures against five US-linked firms.

- China Transport Ministry said it opened an investigation into the impact of US 301 tariffs on China's shipping industry.

- China's Commerce Ministry urges the US to correct mistakes and hopes to resolve concerns through dialogue.

- China increases oversight of export license applications for rare earth magnets, via Reuters citing sources.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.4%) are broadly lower across the board, with sentiment hampered by the ongoing US-China spat; overnight, China's MOFCOM announced that it is taking countermeasures against five US-linked firms.

- European sectors hold a strong negative bias. Telecoms takes the top spot, boosted by post-earning strength in Ericsson (+13%) after it beat on profits and raised guidance. To the bottom of the pile resides Basic Resources, hampered by broader weakness in underlying metals prices.

- US equity futures (ES -0.8%, NQ -1.1%, RTY -0.9%) are lower across the board, following a similar theme seen in Europe. All focus today on a number of bank results, to kick off Q3 earnings seasons.

- BP (BP/ LN) Q3'25 Trading Statement: Upstream Production in Q3 is now exp. to be higher vs prior quarter, but flagged weaker trading into Q3.

- BlackRock Inc (BLK) Q3 2025 (USD): Adj. EPS 11.55 (exp. 11.24), Revenue 6.51bln (exp. 6.23bln); AUM 13.464tln (exp. 13.37tln).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- After a soft start to the session, whereby DXY was dragged lower by the haven bid into the JPY, the Greenback was able to garner support at the expense of risk-sensitive currencies and the GBP (post-jobs data). The bout of risk aversion was triggered by China's decision to take countermeasures against five US-linked firms - a move which has dashed some of the hopes seen during yesterday's session. Furthermore, a source piece in the WSJ overnight stated that "people close to the Trump administration say the US side likely will demand that China rescind, not merely delay or water down the rare-earth export rule". Focus today on US NFIB Small Business Optimism index, and speakers include Fed Chair Powell, Waller, Collins & Bowman. DXY has ventured as high as 99.47, with the next target coming via last week's peak at 99.56.

- After initially looking like it was going to make a test of 1.16 overnight, EUR/USD was dragged lower by the broader pick-up in the USD. From a macro perspective, focus in the Eurozone remains on France with PM Lecornu set to present his budget at 14:00 BST, aiming to reduce the deficit to 4.7% by end-2026. In terms of the specifics, Politico reports that additional measures to those previously expected will include a tax on the richest members of society. Even with the Socialists on board, the governing coalition would still need to find additional votes in the Assembly, which looks tough given that the Far Right and Left are expected to table a no-confidence motion on Lecornu. Elsewhere in core Europe, German ZEW data showed misses for both metrics, with the current conditions component slipping further into negative territory. EUR/USD has been as low as 1.1543 and is just about holding above last week's low at 1.1542.

- JPY is the only of the majors to out-muscle the USD given its safe-haven status. JPY was supported in early European trade as investors reacted to the increase in US-China tensions overnight (see USD section for details). Subsequently, USD/JPY was dragged as low as 151.63 vs. an earlier session high at 152.61. A pick-up in the USD has since seen the pair return to a 152 handle. In terms of the macro story for Japan, it is one that remains dominated by domestic politics following the collapse of the ruling coalition. Note, the LDP party has proposed October 21st for an extraordinary Diet session.

- GBP was hit in early European trade following the latest UK labour market report, which was largely viewed with a dovish lens. Surmising the data, Pantheon Macroeconomics highlighted the unexpected uptick in the unemployment rate and the decline in 3M/YY ex-bonus average earnings, which will factor into thinking on the MPC. Elsewhere, BRC retail sales slowed to 2.0% Y/Y in September from 2.9% as consumers remain cautious in the run-up to next month's fiscal event. Cable has delved as low as 1.3255 to levels not seen since early August.

- Antipodeans are both are softer vs. the USD and at the bottom of the G10 leaderboard. In the absence of any material domestic updates, AUD and NZD remain at the whim of broader risk dynamics, which are being led by US and Chinese trade tensions.

- Click for a detailed summary

FIXED INCOME

- USTs are bid, firmer by over 10 ticks to a 113-16+ high. Strength this morning comes on the back of the downbeat risk tone as China retaliates. Upside that has driven the benchmark to a fresh high for the month, with the next points of resistance at 113-21, 113-25+ and then the 113-29 September peak. Specifically, China's MOFCOM announced that it is taking countermeasures against five US-linked firms and outlined that the US cannot have talks while new restrictions are being threatened. Elsewhere, the docket is packed with Fed speak via voters Bowman, Waller, Chair Powell and 2025 voter Collins.

- OATs are firmer today, in-fitting with peers. A packed agenda for French politics. The main update this morning came from the French fiscal watchdog HCFP on the 2026 budget draft, a draft that was in-fitting with overnight sources. On the draft, HCFP described it as relying on overly optimistic scenarios and ambitious spending restraint that would be difficult to implement. Perhaps most pertinently today, PM Lecornu’s General Policy Statement is scheduled for 14:00 BST. The statement should take no more than 90 minutes, afterwards other party leaders can respond. It is worth highlighting that the French Socialist Party will not vote against PM Lecornu's government, and instead opt for its own motion of no confidence, if it not satisfied with the proposal.

- Bunds are bid, given the market narrative outlined in USTs. No move to final German HICP for September this morning which was unrevised. For Bunds, the morning’s main event was October ZEW. The series came in softer than expected across the board and sparked some modest upside in Bunds

Comments

In Channel

Download from Google Play

Download from App Store

United States

United States00:00

00:00

x