US Market Open: US equity futures mixed, USD pauses as market awaits ADP and ISM data

Update: 2025-11-05

Description

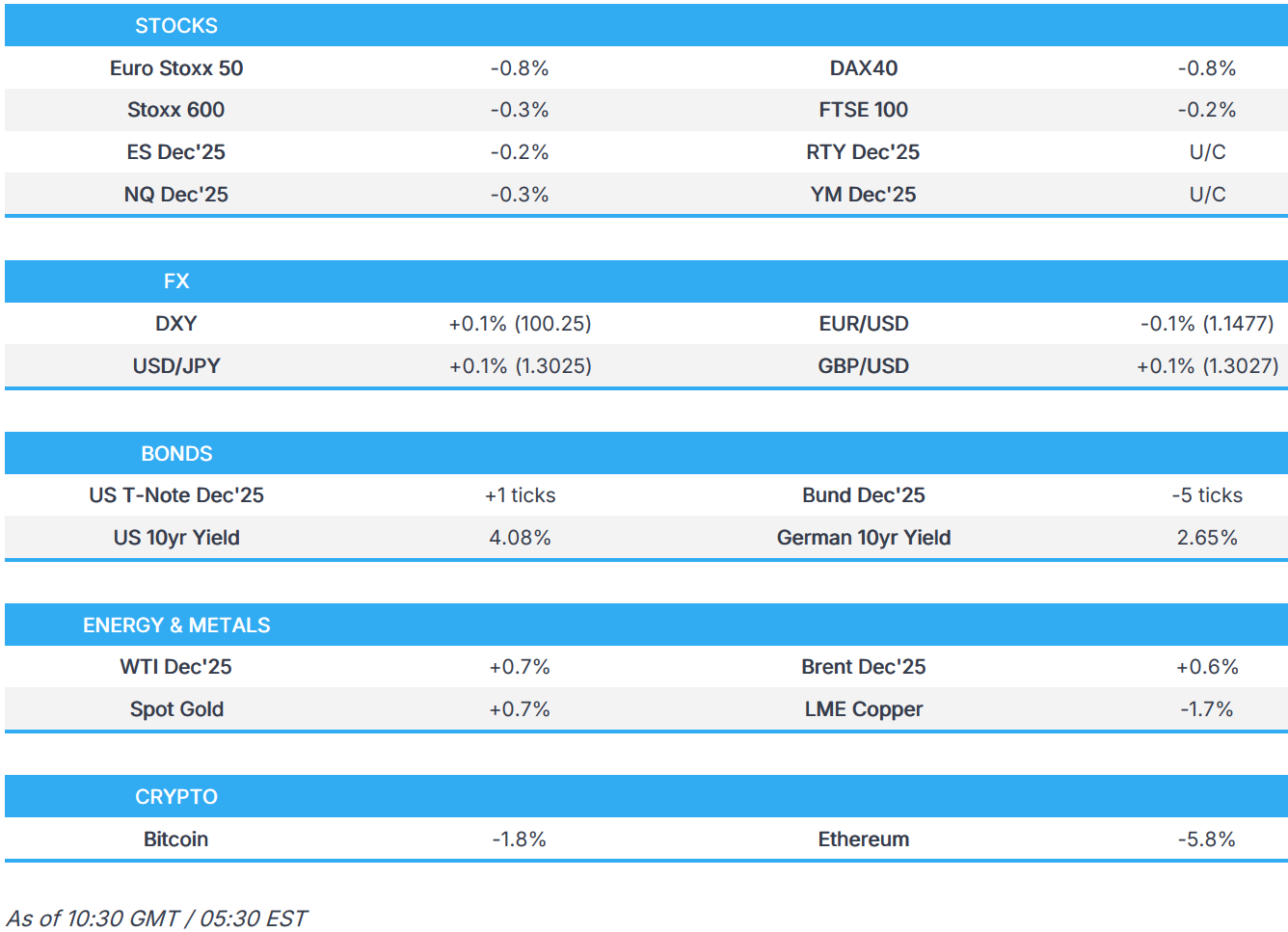

- European bourses are entirely in the red; US equity futures mixed, with the NQ continuing to underperform whilst the RTY takes a breather.

- Recent USD rally pauses for breath ahead of ADP and ISM services.

- USTs are contained into a packed agenda, Gilts continue to ease from Tuesday's best.

- Commodities rebound following Tuesday’s risk-off sell-off.

- Looking ahead, highlights include US Final PMI, US ADP, US ISM Services PMI, NBP & BCB Policy Announcements, US Supreme Court Tariff hearing begins, Speakers including BoE's Breeden, BoC's Macklem & Rogers, US QRA. Earnings from AMC, Arm, Snap & McDonald’s.

</figure>

</figure>TARIFFS/TRADE

- US President Trump posted the "United States Supreme Court case is, literally, LIFE OR DEATH for our Country. With a Victory, we have tremendous, but fair, Financial and National Security. Without it, we are virtually defenceless against other Countries who have, for years, taken advantage of us. Our Stock Market is consistently hitting Record Highs, and our Country has never been more respected than it is right now. A big part of this is the Economic Security created by Tariffs, and the Deals that we have negotiated because of them."

- US President Trump posts it was his "Great Honor to just meet with high level Representatives of Switzerland. We discussed many subjects including, and most importantly, Trade and Trade Imbalance. The meeting was adjourned with the understanding that our Trade Representative, Jamieson Greer, will discuss the subjects further with Switzerland’s Leaders."

- White House posted the Executive Order modifying duties addressing the synthetic opioid supply chain in China.

- White House said it is not interested in selling to China at this time regarding NVIDIA (NVDA) Blackwell chips.

- China announced it will suspend 24% US tariffs for a year but will maintain 10% US tariffs, while it will lift some tariffs on US agriculture goods from November 10th.

- Chinese Premier Li said some unilateral and protectionist measures have had severe impacts on the economic world order, while he said they should uphold equality and mutual benefit and consolidate the foundation of legitimate common interest. Li stated that it is all the more important for them to stay committed to mutual cooperation and pursue free trade when economic growth is slowing. Furthermore, he said China is willing to stand with all parties to foster an open and inclusive environment, as well as commented that countries should not seek unilateral wins at the expense of others, and need to balance their interests against the greater good.

- White House said US President Trump feels positively about the relationship with India and trade teams continue to be in serious discussions, while it added that President Trump and Indian PM Modi speak frequently.

- China Commerce Ministry suspends unreliable entity list announced in April; removes entity list announced in March and will adjust the list.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.2%) opened entirely in the red, as the downbeat risk tone continues to follow through into today's session. Lack of pertinent newsflow and a slew of EZ PMIs have had little impact to change price action, which has been fairly rangebound throughout the day.

- European sectors hold a negative bias. Autos takes the top spot, buoyed by post-earning strength in BMW (+1.5%) after reporting decent Q3 metrics, and reiterating its FY outlook. Tech is found towards the foot of the pile, as AI-bubble fears continue to grow; ASML (-2%). Elsewhere, Novo Nordisk (+1%) has pared initial losses, despite poor headline metrics and trimming FY guidance.

- US equity futures (ES -0.2%, NQ -0.3%, RTY U/C) are mixed, as the ES/NQ continue to extend on recent pressure whilst the RTY pauses for breath. Today's focus will be on the US ADP figures, which has increased focus given the suspension of the NFP report, amidst the US gov't shutdown; US ISM Services are also on the docket.

- China bans foreign AI chips from state-funded data centres, via Reuters sources; likely to affect US chipmakers such as NVIDIA (NVDA), AMD (AMD), Intel (INTC); foreign chips banned in Chinese state-funded data centres include NVIDIA H20, B200 and H200.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- The recent rally in the USD that has been driven by improving US-China relations, the hawkish FOMC announcement and yesterday's global equity selling has paused for breath. As the US shutdown enters its 35th day, matching its prior record, official US data releases remain suspended. However, today we will be presented by the latest ADP employment report and ISM services print. The former is expected to see employment in October rise to 28k from the -32k print in September. For the ISM print, consensus looks for the headline metric to pick-up to 50.8 from the neutral 50 mark. Elsewhere, today will see the commencement of the hearing on the legality of US President Trump's Reciprocal Tariff Policy. DXY remains below Tuesday's best at 100.25.

- EUR is attempting to stop the rot vs. the USD following a recent run of losses, which dragged EUR/USD down from a 1.1668 peak last week to a 1.1473 trough yesterday. Incremental macro drivers remain on the light side for the Eurozone with final services & composite PMIs and an unrevised ECB annual wage tracker failing to move the dial for the EUR.

- JPY is now only incrementally firmer vs. the USD following a bout of strength overnight as global equities continued to slip. USD/JPY delved as low as 152.97 before returning to levels above 153.50. Recent strength in JPY has been stemming more from the risk-aversion price action in the market as opposed to anything Japan-specific. Fleeting modest JPY appreciation was seen in early European trade after Japanese Top Currency Diplomat Mimura noted that recent JPY moves are deviating from fundamentals and that excessive FX volatility, not levels, is the main concern.

- GBP is attempting to atone for its recent run of losses, which have largely been driven by increasing odds of a December BoE cut and ongoing angst ahead of the November 26th budget. This angst was brought to the forefront yesterday following Chancellor Reeve's pre-budget speech in which she stopped shy of naming any specific policies but helped reaffirm the markets view that it will be a growth-negative event. Cable is holding above Tuesday's 1.3010 trough but some way off the 1.3139 peak.

- Antipodeans are mixed, with the Kiwi marginally outmuscling the Aussie on the cross. Overnight markets had Chinese Services/Composite PMI data, in which the former marginally topped estimates, but the composite figure slowed. Overall, quiet trade for the pair this morning, as the FX space awaits key US data.

- As was widely-expected, the Riksbank opted to keep rates unchanged and reiterated guidance that the "policy rate is expected to remain at this level for some time to come". Within its economic assessment, it was judged that the outlook for inflation and economic activity remains largely unchanged. SEK was little moved.

- PBoC set USD/CNY mid-point at 7.0901 vs exp. 7.1336 (Prev. 7.0885)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- A firmer start to the day for USTs but only modestly so. Action for USTs overnight occurred in tandem with the broader risk tone, as a move lower in equity futures was seen around the beginning of the APAC session, the fixed benchmark picked up, taking USTs to an overnight 113-02 high. Thereafter, the benchmark drifted as the risk tone picked up off lows and stabilised. Nonetheless, USTs hold onto modest gains but are at the lower-end of a narrow 112-26 to 113-02 band. The docket ahead is packed from a US perspective. On the data front, the monthly ADP (reminder, they also do a weekly update now on non-NFP weeks) series is due and expected to come in at 28k (prev. -32k); ISM Services also due. The Quarterly Refunding Announcement is also due and is expected to maintain the nominal coupon auction sizes for the November-January period. Finally, the Supreme Court tariff hearing begins today with oral arguments to be presented for the first time.

- Bunds are echoing USTs in terms of overnight direction, though the magnitude o

Comments

In Channel

Download from Google Play

Download from App Store

United States

United States00:00

00:00

x