Europe Market Open: European equity futures mostly lower taking cues from Wall St; Flash PMI from UK and EZ ahead

Update: 2025-11-21

Description

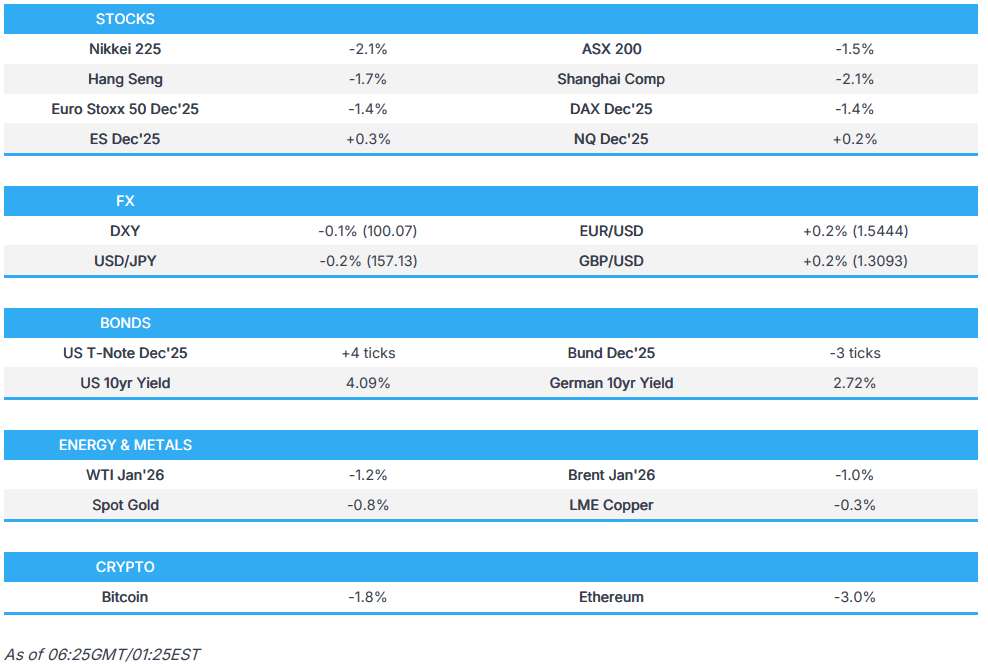

- APAC stocks traded lower across the board as the sharp Wall Street selloff reverberated through the region despite the absence of fresh catalysts.

- JPMorgan no longer expects the Federal Reserve to cut rates in December, vs its prior forecast of a 25bp cut.

- 10yr JGB futures retraced some of this week's losses whilst the session saw a slew of commentary from Japanese Finance Minister Katayama, who, on the bond market, attempted to alleviate some fiscal woes.

- Japan may intervene before USD/JPY reaches 160, according to Bloomberg, citing a government panellist.

- Crypto markets continue bleeding with Bitcoin falling under USD 85,500 at a 7-month low, while Ethereum fell to a 4-month low.

- Looking ahead, UK PSNB (Oct), Retail Sales (Oct), EZ, UK & US Flash PMIs (Nov), US Real Weekly Earnings (Sep), Canadian Retail Sales (Sep), US Uni. of Michigan (Nov), Euro Area Indicator of Negotiated Wage Rates (Q3), Moody’s on the UK & Italy, ECB’s de Guindos, Lagarde, Nagel; Fed’s Williams, Barr, Jefferson, Logan; SNB’s Schlegel.

- Click for the Newsquawk Week Ahead.

</figure>

</figure>US TRADE

EQUITIES

- US stocks ended with heavy selling. Initially, markets saw notable risk on sentiment, with US indices seeing extensive gains, high beta FX outperforming, and the crude complex strengthening, which came after a stellar NVIDIA (NVDA) report and guidance. Thereafter, markets turned, although the risk-off had no fresh driver. AI valuations remain a concern, even after the strong NVDA report, while Goldman Sachs warned Wednesday of USD 39bln in equity sales from trend-following hedge funds after the SPX fell to sub 6,725 on Monday.

- SPX -1.56% at 6,539, NDX -2.38% at 24,054, DJI -0.84% at 45,752, RUT -1.82% at 2,305.

- Click here for a detailed summary.

NOTABLE HEADLINES

- US Treasury Secretary Bessent said the Fed should keep going with its cutting cycle and should be looking at the data, via Bloomberg.

- Fed’s Goolsbee (2025 voter) said part of the Fed’s job is to be the steady hand, noting that the Fed set a 2% inflation target and that 3% inflation is too high, calling the 2% goal a sacred promise. He said inflation seems to have stalled and that he is a little uneasy about inflation, uneasy about front-loading rate cuts, and uneasy about relying on “transitory” inflation. He said official data is a mess because “the lights went out,” and that in the dark he was more paranoid about inflation due to less available information. Goolsbee noted a notable slowdown in job creation but said he is dubious that the payroll slowdown points to recession; he described the current low-hiring, low-firing environment as a sign of uncertainty. He said the boom in data centres makes it harder to gauge the business cycle, warned that AI investment raises concerns about a possible bubble, and said 50-year mortgage rates could reduce the impact of monetary-policy decisions, according to Reuters.

- Fed’s Goolsbee (2025 voter) reiterated he is uneasy about front-loading rate cuts before knowing whether the inflation uptick is transitory. He said he is not hawkish over the medium term and believes rates will ultimately settle well below current levels. After the Fed’s September cut he felt just one more cut would be needed for 2025, and when he voted for the October cut he assumed the job market was cooling gradually.

- Fed’s Cook (voter) said not all market volatility is problematic, adding that one major vulnerability is maturity mismatch in hedge-fund Treasury-securities trading strategies, according to Reuters.

- Fed’s Paulson (2026 voter) said she is approaching the December rate decision cautiously and that the September labour-market report was encouraging overall, though she remains, on balance, more worried about the labour market than inflation. She said rate cuts so far have been appropriate but each one raises the bar for the next, and with upside risks to inflation and downside risks to employment, monetary policy must walk a fine line. She expects to learn a lot between now and the December meeting and said her longer-term policy thinking is focused on balancing inflation and labour-market risks. Paulson said the US economy is doing OK, but aggregate growth is unusually dependent on high-income earners and is particularly sensitive to equity valuations. She added that tariff effects are smaller than feared and that the overall demand environment is helping contain inflation, according to Reuters.

- JPMorgan no longer expects the Federal Reserve to cut rates in December, vs its prior forecast of a 25bp cut.

- OpenAI CEO Sam Altman is bracing for possible economic headwinds in catching up to a resurgent Google (GOOGL), according to The Information. He told colleagues last month that Google’s recent AI progress could “create some temporary economic headwinds” for OpenAI, and the company’s narrowing tech lead and rising cash-burn projections have raised questions among investors.

DELAYED DATA UPDATE

- Federal Reserve scheduled Industrial Production and Factory orders data for 3rd December at 09:15 EST/14:15 GMT.

DATA RECAP

- US 30-year fixed rate mortgage (Nov 20th): 6.26% (prev. 6.24%)

TRADE/TARIFFS

- US President Trump signed an order modifying the scope of tariffs on Brazil, stating that certain agricultural products will not be subject to the additional ad valorem duty imposed under Executive Order 14323, according to the White House. Bloomberg reported that Trump has expanded his reductions of certain food tariffs by extending them to the 40% surcharge placed on Brazil over the Bolsonaro case, noting that last week’s exemptions did not apply to that portion of the tariffs. White House said US President Trump's order on Brazilian imports removes tariffs announced on July 30th on imports of Brazilian beef, coffee, and orange juice.

- EU Trade Commissioner said momentum is improving on the Australia–EU trade deal and expects another round of talks early next year, according to Reuters.

APAC TRADE

EQUITIES

- APAC stocks traded lower across the board as the sharp Wall Street selloff reverberated through the region despite the absence of fresh catalysts.

- ASX 200 was dragged down by all sectors, with gold and mining leading declines; tech held up relatively better alongside defensive names.

- Nikkei 225 slipped at the open, pressured by mining and metals, while financials found some relief as yields eased off highs. No move was seen on the budget, which came in line with expectations.

- Hang Seng and Shanghai Comp both opened softer but recovered to trade firmer, though still reflecting the cautious global tone.

- US equity futures consolidated after Thursday’s heavy selloff, with the ES finding support around 6,550 and the NQ stabilising near the 24,000 area.

- European equity futures are indicative of a lower cash open with the Euro Stoxx 50 -1.5% after cash closed +0.3% on Thursday.

FX

- DXY held flat in a tight 100.08–100.22 band amid a lack of fresh overnight drivers, following a relatively stable Thursday session despite the equity sell-off. The index stayed comfortably within yesterday’s 100.02–100.36 parameters.

- EUR/USD was uneventful in a quiet session with no major catalysts as traders positioned ahead of the Eurozone Flash PMIs.

- GBP/USD remained capped below 1.3100, with UK-specific newsflow light and caution setting in ahead of next week’s Budget. UK Retail Sales and Flash PMIs were in focus to close out the week.

- USD/JPY was choppy within a tight range between 157.10-157.54 despite extensive verbal intervention from Japanese Finance Minister Katayama, who suggested that they take appropriate action if FX moves excessively, whilst FX intervention is an option. Meanwhile, Japanese CPI printed in line while Flash PMIs flagged that "Inflation remains a key concern, however, with average input costs rising at the quickest rate in six months amid reports of higher labour costs and supplier price hikes. As a result, firms raised their own selling prices at a solid pace, as they looked to protect their margins."

- Antipodeans narrowly outperformed in the G10 space following the prior session's underperformance, with little movement seen on the New Zealand Trade Balance and Australian Flash PMIs.

- PBoC set USD/CNY mid-point at 7.0875 vs exp. 7.1154 (Prev. 7.0905)

FIXED INCOME

- 10yr UST futures were holding a mild upward bias and retaining most of yesterday's gains amid the broader risk aversion in Asia.

- Bund futures were flat/subdued despite the broader risk

Comments

In Channel

Download from Google Play

Download from App Store

United States

United States00:00

00:00

1.0x